Γίνετε μέλος μιας κοινότητας βιβλιόφιλων από όλο τον κόσμο και επωφεληθείτε από πολλά προνόμια.

Δημιουργία δωρεάν λογαριασμού

Δωρεάν αποστολή με Box Now άνω των 69.99 €

DHL courier 9.99 €

Σημείο Elta 3.99 €

Elta 4.49 €

ACS 4.99 €

Σημείο ACS 4.99 €

Box Now 3.99 €

Επικοινωνία

Επικοινωνία Πώς να κάνετε αγορές;

Πώς να κάνετε αγορές;

Βοήθεια

Παράδοση

DHL courier 9.99 €

Σημείο Elta 3.99 €

Elta 4.49 €

ACS 4.99 €

Σημείο ACS 4.99 €

Box Now 3.99 €

Δωρεάν αποστολή με Box Now άνω των 69.99 €

Οδηγός αγορών

Είμαστε στη διάθεσή σας!

210 2602819

Ο λογαριασμός μου

▸

Άδειο :-(

0

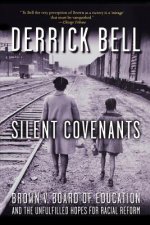

Multi-factor Models and Signal Processing Techniques

Application to Quantitative Finance

Γλώσσα

Αγγλική

Αγγλική

Αγγλική

Βιβλίο

Σκληρόδετο

Multi-factor Models and Signal Processing Techniques surveys the most widely used factor models emp...

Πλήρης περιγραφή

Κωδικός Libristo: 05103670

?

430 b

430 b

430 b

177.74

€

Εξωτερικός αποθηκευτικός χώρος

Αποστέλλουμε σε 9-15 ημέρες

Παράδοση στην Ελλάδα

Παράδοση στην Ελλάδα

Παράδοση στην Ελλάδα

30 ημέρες για την επιστροφή των προϊόντων

Οι πελάτες αγόρασαν επίσης

/

/

Σκληρόδετο

Σκληρόδετο

207.25

€

207.25

€

Multi-factor Models and Signal Processing Techniques surveys the most widely used factor models employed in the realm of the financial asset pricing field. It offers a unique perspective on these models, using the concrete application of evaluating risks in the hedge fund industry to demonstrate that signal processing techniques can be an interesting alternative to the selection of factors, whether they are fundamental or statistical factors. More importantly, the book shows how the signal processing approach can provide more efficient estimation procedures based, for instance, on lq regularized Kalman Filtering.

Ηθοποιός

&

Πολύγλωσση

EWA KASP

για

Αναπαραγωγή βίντεο

το Libristo διαθέτει τη μεγαλύτερη επιλογή ξενόγλωσσων βιβλίων. Γι' αυτό αγοράζω τα βιβλία μου εδώ.

Πληροφορίες για το βιβλίο

Πλήρες όνομα

Multi-factor Models and Signal Processing Techniques

Συγγραφέας

Serges Darolles, Patrick Duvaut, Emmanuelle Jay

Γλώσσα

Αγγλική

Αγγλική

Βιβλιοδεσία

Βιβλίο - Σκληρόδετο

Ημερομηνία έκδοσης

2013

Αριθμός σελίδων

182

EAN

9781848214194

ISBN

1848214197

Κωδικός Libristo

05103670

ΕΕκδοτικός οίκος

ISTE Ltd and John Wiley & Sons Inc

Βάρος

488

Διαστάσεις

157 x 239 x 21

Χαρίστε αυτό το βιβλίο σήμερα

Είναι εύκολο

1 Προσθέστε το βιβλίο στο καλάθι σας και επιλέξτε παράδοση ως δώρο 2 Ως ανταμοιβή θα σας στείλουμε ένα κουπόνι 3 Το βιβλίο θα φτάσει στη διεύθυνση του παραλήπτηΜπορεί να σας ενδιαφέρει

/

Χαρτόδετο

33.14

€

/

Χαρτόδετο

33.14

€

/

Χαρτόδετο

48.90

€

/

Χαρτόδετο

48.90

€